Radiology Maintains Dominant Position in Medical AI

The Food and Drug Administration (FDA) has released an updated list of AI-enabled medical devices, confirming that radiology continues to overwhelmingly dominate the authorization landscape. With data covering through the end of December 2025, the agency has now recorded a total of 1,451 authorized AI devices since tracking began in 1995 — of which an impressive 1,104, or 76%, belong to radiology.

Fourth Quarter 2025 by the Numbers

In the fourth quarter of 2025 alone, the FDA cleared 72 new AI-enabled medical devices, with 55 of them — again 76% — focused on radiology applications. For the full year of 2025, the specialty secured 75% of all authorizations, compared to 73% in 2024 and 80% in 2023. While AI applications in other medical fields continue to grow, radiology remains the primary field for technological innovation.

The first radiology device on the FDA’s list dates back to 1998, when R2 Technology’s (now Hologic) ImageChecker received authorization. Since then, growth has been exponential, particularly from 2018 onward, when deep learning adoption drove a new wave of solutions for AI-assisted detection in diagnostic imaging.

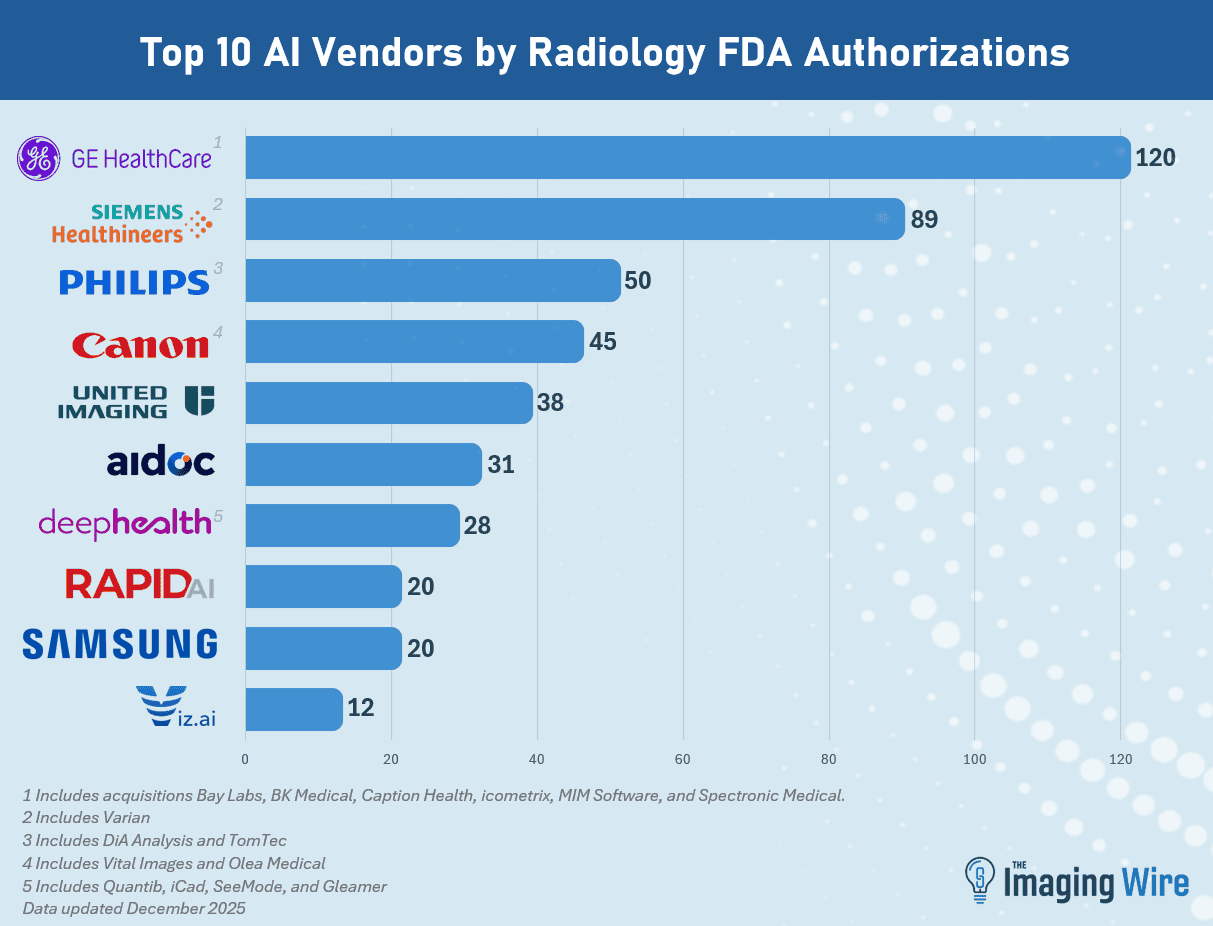

Manufacturer Rankings in Radiological AI

Market consolidation in radiological AI becomes evident when analyzing the manufacturer rankings. GE HealthCare leads with 120 authorizations, a figure that includes acquisitions of companies such as Bay Labs, Caption Health, MIM Software, and icometrix. The company has been showcasing AI leadership at HIMSS 2026, further cementing its position atop the rankings.

Following GE are Siemens Healthineers with 89 authorizations (including Varian), Philips with 50 (including DiA Analysis and TomTec), Canon with 45 (including Vital Images and Olea), United Imaging with 38, Aidoc with 31, and DeepHealth with 28 (including Quibim and iCAD). The intense M&A activity demonstrates the market is in a phase of accelerated consolidation.

Market Consolidation and Clinical Impact

The FDA’s list includes not only standalone software applications but also imaging hardware with embedded AI — such as portable X-ray systems with algorithms for detecting emergent conditions. This convergence of hardware and AI software is transforming the radiological workflow by automating triage and prioritization of critical examinations.

The consolidation trend carries significant implications for healthcare systems worldwide. As major players acquire AI startups, access to these technologies is becoming more tightly integrated into existing radiology information systems, including PACS and reporting platforms. Professionals who stay abreast of these developments will be better prepared for adopting these tools in their daily routines.

Outlook for 2026 and Beyond

Expectations point to a continued rapid pace of authorizations in 2026, driven by advances in large language models applied to radiological reports, generative AI for image reconstruction, and autonomous triage solutions. The recent approval of AI-based risk assessment systems for mammography indicates that the scope of applications will continue expanding beyond detection into prediction and risk stratification.

The landscape points toward a future where AI does not replace the radiologist but integrates deeply into the workflow, enabling professionals to focus their expertise on the most complex cases while algorithms handle automated triage and quantification.

Source: The Imaging Wire